Intro — Why this matters now

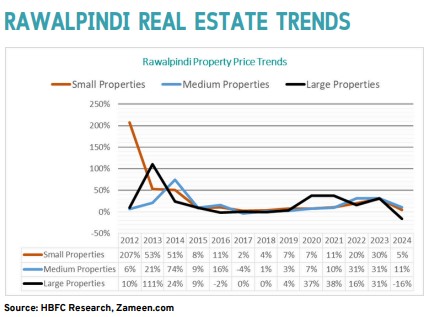

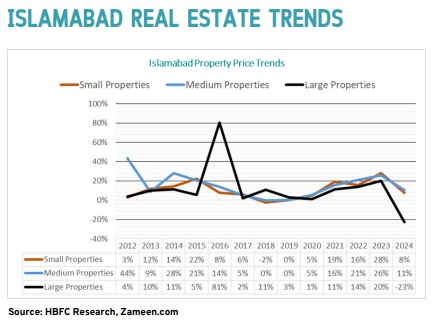

Over the last decade, the Islamabad-Rawalpindi real-estate market has shown cycles of strong growth, episodic corrections, and concentrated surges in specific projects (Bahria Town, DHA, Capital Smart City). For buyers and investors, the central question is simple: Does waiting cost you money? The short answer: yes — in many submarkets, delaying even a single year has translated into substantial unseen opportunity cost. A number of market reports and listing platforms show that major, well-managed projects have outperformed general markets and often show fast appreciation after infrastructure milestones.

Quick snapshot (what happened 2016 → 2025)

-

2016–2018: Early boom in large/developer-backed projects (notably DHA and some Bahria blocks).

-

2019–2021: A pause and localized corrections in several pockets; buyers switched toward ready/possession properties and smart-city launches.

-

2022–2024: Renewed increase—large projects and well-located plots saw double-digit annual gains; some Bahria blocks and DHA pockets spiked.

-

2025 (early): Continued momentum in select suburbs and smart city zones, while some fringe speculative pockets stayed flat.

Key evidence sources: HBFC research summary and Zameen / market trackers for Bahria & DHA listings.

Major areas & 10-year behavior (high-level)

1) Bahria Town (Rawalpindi)

Bahria Town has been a top performer when infrastructure milestones (new roads, commercial rollouts) were delivered; recent site prices show steady appreciation and continued buyer interest for ready/near-possession plots. For area-level averages, see the listing platform.

2) DHA (Islamabad / Rawalpindi)

DHA pockets (especially those in developed phases) have shown strong cumulative growth since 2016, with clear upward jumps around handover/utility milestones. DHA remains premium and thus resilient in corrections. Listing history from property portals shows substantial long-term gains.

3) Capital Smart City

Smart-city launches created an earlier lower-price entry point (2018–2020) that appreciated once construction and connectivity announcements matured — a classic infrastructure → price effect.

4) Bahria Enclave, Mumtaz City, Faisal Town

These established & semi-developed neighborhoods show steady, moderate growth; they spike when new commercial anchors or road links are announced. Local brokers’ price feeds indicate consistent demand for possession-ready plots.

5) CDA Sectors (B17) / Multi Gardens / E & F sectors

CDA-designated sectors and low-rise suburbs performed variably; some pockets lagged, but B17 and similar sectors gained after infrastructure upgrades and improved road links. FBR Download+1

Where the spikes & declines happened (years & triggers)

Below are principal spike years and typical causes (illustrative, compiled from market trackers & research reports):

-

2016 — initial developer price surges in large projects (early buyers in new phases saw major gains).

-

2019–2020 — pockets of slowdown due to macro & liquidity pressures; opportunistic buyers entered smart city launches.

-

2021–2023 — strong rebound as construction resumed, handovers completed, and speculation returned (many Bahria & DHA blocks recorded noticeable spikes).

-

2024 — mixed: some high-demand submarkets cooled slightly; others continued to rise, especially ready-to-build plots in premium sectors.

These observations are supported by HBFC and commercial portal snapshots showing cyclical highs and recoveries.

Not sure which area will give you the highest return in the next 5–10 years?

Let us create a free personalized investment plan based on your budget and goals.

Visit: www.rahbarestateconsultants.com

📩 Email: guide@rahbarestateconsultants.com

📞 Call/WhatsApp: +92 333 568 3992Rahbar Estate Consultants – Guiding You with Honesty & Clarity

Join The Discussion